Practice Exam Questions

Minimum Alcohol Pricing (Revision Essay Plan)

- Level:

- AS, A-Level, IB

- Board:

- AQA, Edexcel, OCR, IB, Eduqas, WJEC

Last updated 10 Dec 2018

Here is a suggested answer to a question on minimum price for alcohol. "Assess the view that a minimum price on alcohol is likely to be an effective and equitable intervention to curb externalities from drinking."

Essay Minimum Alcohol Price (Download a pdf version of this essay plan)

Brief Introduction

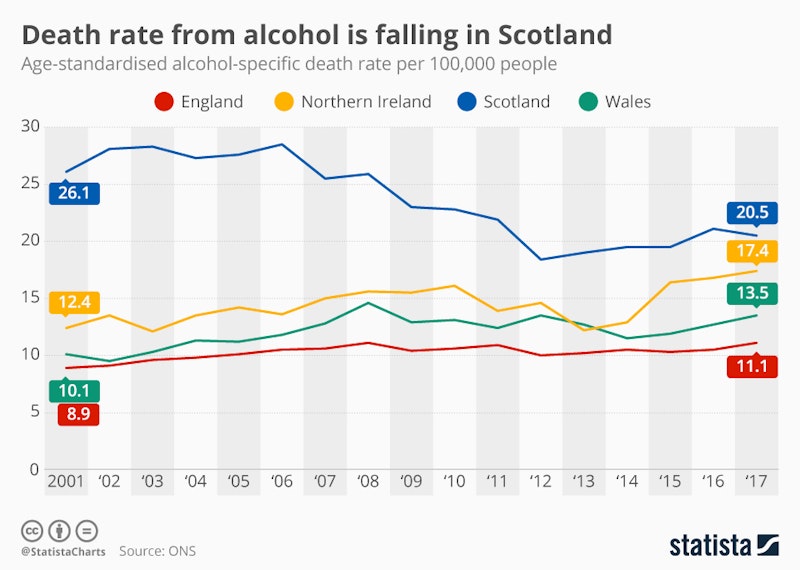

A minimum price of 50 pence per unit has been introduced in Scotland from 1st May 2018 but not in England where the government has chosen to introduce a ban on selling alcohol under a “permitted price” which means that a can of average strength lager cannot be sold for less than 41p and a standard bottle of vodka cannot be sold for less than £9.06. This essay will assess whether imposing a legal price floor is likely to work and also be equitable to different stakeholders.

Point 1

The first argument for having a minimum price on alcohol is that excessive drinking leads to negative externalities from consumption which is a major cause of market failure and leads to significant social costs. Anti-social behaviour associated with binge drinking impacts not just those who over-consume but impose external costs on the health service and uses up the scarce resources of the police and criminal justice system. Alcohol abuse can also lead to increased absenteeism from work and lower labour productivity in the long run. The effect of negative externalities is shown in my analysis diagram where marginal social cost exceeds marginal private cost leading (in the absence of any intervention) to a deadweight loss of social welfare. A research report from the University of Sheffield estimated the following annual costs arising from alcohol mis-use: NHS costs £3.5 bn, alcohol-related crime £11 bn and lost productivity due to alcohol £7.3 bn. In this situation, some form of government intervention is clearly justified and the Scottish government argues that a minimum price floor is better for targeting harmful binge drinking, while leaving the more moderate drinker relatively unaffected. In this sense, it is an equitable policy.

Evaluation of Point 1

However, there is a danger that intervention can lead to one or more government failures. One argument is that putting a minimum price on alcohol will lead to unintended consequences. For example, banning cheap alcohol at festivals and other events might lead young people to switch to using cheaper non-alcoholic drugs instead. If drinkers cannot afford alcohol at legally-imposed minimum prices, they may turn to shadow markets so we might expect a rise in cross-border shopping as consumers go to supermarkets in England to get their alcohol at a cheaper price. If people want to get around a regulation, they will normally find a way do so if there is an obvious net financial benefit.

Point 2

A second argument in favour of minimum unit pricing for alcohol is that enforcing a minimum unit price will encourage drinks manufacturers to reformulate their products so that any price increase for the consumer is limited. For example, in 2012, AB InBev (one of the world’s biggest brewers) reduced the alcohol content of their beers for the UK market, from 5% to 4.8%. They have seen sales rise strongly in recent years suggesting that focusing on lower-strength beers and zero-alcohol drinks might generate supernormal profits in the long run. A minimum unit price for alcohol could have similar effects to what we have seen occur with the phrased introduction of a sugar tax where many firms have moved quickly to reduce the sugar content of drinks to reduce their liability to pay tax. Reformulation helps lower the risks of alcohol-fueled violence and therefore can be a justified intervention in the market.

Evaluation of Point 2

Critics of the minimum alcohol price counter by saying that it is a tax on responsible drinkers and that many families on average or below-average incomes will be badly affected. Research from the Institute of Fiscal Studies has found that 5% of households in the UK buy more than 30% of all alcohol. Why should people who drink in moderation have to pay a higher price? A legally enforced minimum price might be seen as having a regressive effect on poorer households. The wine and spirits industry has lobbied against the Scottish minimum price arguing that it is inconsistent with the operation of the free market for the state to intervene on price and that it is a barrier to trade. They claim that lower sales of alcoholic drinks will cost jobs in the UK, both from manufacturing and from reduced revenues of corner shops, pubs and other retailers.

Point 3

A third argument in favour of minimum unit pricing for alcohol focuses on the actual behaviour of consumers. One cause of alcohol-related violence comes from people “preloading” drinks at home before they head out to pubs and clubs. A minimum price for beers and spirits sold in supermarkets would help to curb drinking at home because the marginal private cost of doing so has increased. In my analysis diagram below, we see how a higher price will cause a contraction of demand, the size of which depends on the price elasticity of demand for different drinks. The level of consumer surplus falls as a result. A possible positive spillover from an end to super-cheap alcohol available from supermarkets is that more people will choose to go to pubs instead, perhaps helping to reverse the pattern of pub closures seen for a number of years.

Evaluation of Point 3

Although in theory higher prices will limit demand and consumption, in practice consumers will always find ways around a regulation. One effect might be an increase in home-brewing of beer, gin and wine which might then lead to a rise in alcoholic poisoning and additional external costs. Youngers drinkers in particular might look to get around the legal minimum price by finding illicit alcohol in shadow markets. They are at great risk of suffering the effects of information failure which is another cause of market failure. This is also a policy that could be quite expensive to enforce.

Final reasoned comments

Critics of the minimum price claim that it is both ineffective in changing behaviour and is unfair (inequitable) to responsible drinkers and hits lower income families the most. They also claim that the main effect of the minimum price will be to increase the monopoly profits of the drinks industry at the expense of the consumer welfare of the majority of consumers. Some economists argue that an orthodox indirect tax on alcohol is a better strategy and it also creates tax revenues for the government which can then be earmarked to help fund health and education programmes. Behavioural economists might make the point that nudging consumers - for example by making them more aware of the social consequences of their actions - can be as effective as an intervention in the price mechanism.

Overall, I would argue that a minimum price per unit of alcohol is a justified intervention. Society is waking up to the huge long-term social costs of heavy drinking across all levels of household income. A minimum price is required to reduce consumption closer towards the social optimum and there are signs that it is and will bring about a change in the behaviour both of consumers and producers. The rapid growth of low or zero-alcohol lagers and wines is a reflection of a shift in revealed preferences. The evidence suggests that heavy drinkers tend to buy and consume cheap and high-strength alcohol available away from pubs so this policy could well be quite effective in the years ahead.

Revision Video: Minimum Prices for Alcohol - Evaluation

You might also like

Fiscal Policy (Revision Presentation)

Teaching PowerPoints

The Network Effect Could Sink Labour

21st May 2015

Positive Externalities

Topic Videos

The Dichotomy of Behavioural Economics

15th December 2016