Practice Exam Questions

African Free Trade Agreement (Chain of Analysis)

- Level:

- A-Level, IB

- Board:

- AQA, Edexcel, OCR, IB, Eduqas, WJEC

Last updated 12 May 2019

Examiners want students to build coherent chains of analytical reasoning in their economics papers in order to reach higher levels in the mark scheme. Here is an example on this question: "Examine how a free trade area might stimulate economic growth in Sub-Saharan Africa."

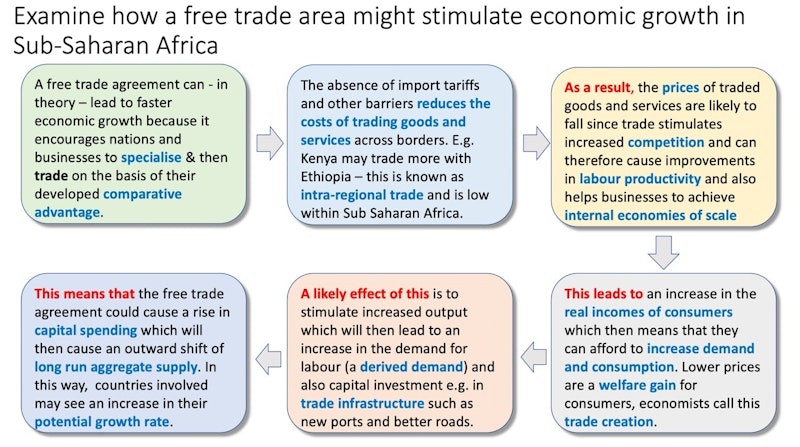

A free trade agreement can - in theory – lead to faster economic growth because it encourages nations and businesses to specialise & then trade on the basis of their developed comparative advantage.

The absence of import tariffs and other barriers reduces the costs of trading goods and services across borders. E.g. Kenya may trade more with Ethiopia – this is known as intra-regional trade and is low within Sub Saharan Africa.

As a result, the prices of traded goods and services are likely to fall since trade stimulates increased competition and can therefore cause improvements in labour productivity and also helps businesses to achieve internal economies of scale

This leads to an increase in the real incomes of consumers which then means that they can afford to increase demand and consumption. Lower prices are a welfare gain for consumers, economists call this trade creation.

A likely effect of this is to stimulate increased output which will then lead to an increase in the demand for labour (a derived demand) and also capital investment e.g. in trade infrastructure such as new ports and better roads.

This means that the free trade agreement could cause a rise in capital spending which will then cause an outward shift of long run aggregate supply. In this way, countries involved may see an increase in their potential growth rate.

Evaluation follows on from the analysis

You might also like

Sources of Comparative Advantage

Study Notes

Sustaining economic growth in Africa

20th December 2014

Beyond the Bike - lesson resource on development in landlocked countries

15th October 2015

Sub-Saharan GDP growth may fall below 2% claims World Bank

30th September 2016

Sunday evening TV and Victorian Economics

20th October 2017

How China plans to lead the computer chip industry

19th November 2019

India’s Obesity Time Bomb

6th November 2023