Study Notes

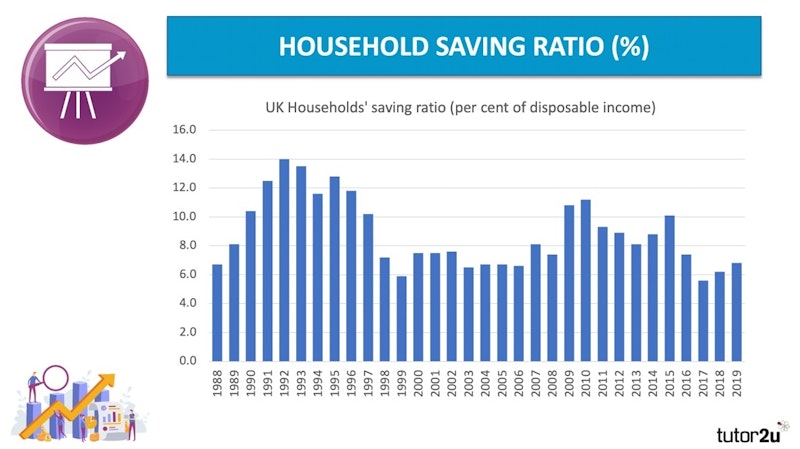

Household Saving

- Level:

- AS, A-Level, IB

- Board:

- AQA, Edexcel, OCR, IB, Eduqas, WJEC

Last updated 27 Oct 2020

Saving is a decision by people to postpone their consumption.

You might also like

Saving in Poor Countries

28th September 2014

60 Second Adventures in Economics - The Paradox of Thrift

20th September 2012

Explaining the Paradox of Thrift

6th October 2009

Monetary and Fiscal Policies Revision Quiz

Quizzes & Activities